After the 2008 Great Financial Crisis, regulations forced European banks to hold more capital against riskier loans. As a result, SME loans became less attractive because they carried similar underwriting and monitoring costs as larger loans but generated lower absolute returns. Private credit firms filled some of the gap but exposed borrowers to floating rates that became unbearable when rates spiked. Now, European SMEs face a €39 billion annual funding gap.

Cointelegraph Research’s new report identifies a structured-access hybrid model within RWA private credit that could help close the funding gap with onchain capital. One platform using this approach has already originated 15.4 million USDC across 2,143 investors.

Read the full Cointelegraph Research report here

RWA Private credit

A key advantage of RWA private credit is fractionalization. In traditional private credit, a single loan position is held entirely by one lender or distributed among a small group of institutional investors through a fund structure. Fractionalization splits the position into smaller units, each representing a proportional claim on the same underlying loan, which makes positions easier to transfer and opens the investor base beyond domestic institutional capital. A retail investor in Indonesia can hold $500 worth of exposure to a Czech SME loan without going through a local broker, custodian, or fund administrator, with settlement clearing instantly through stablecoins across borders.

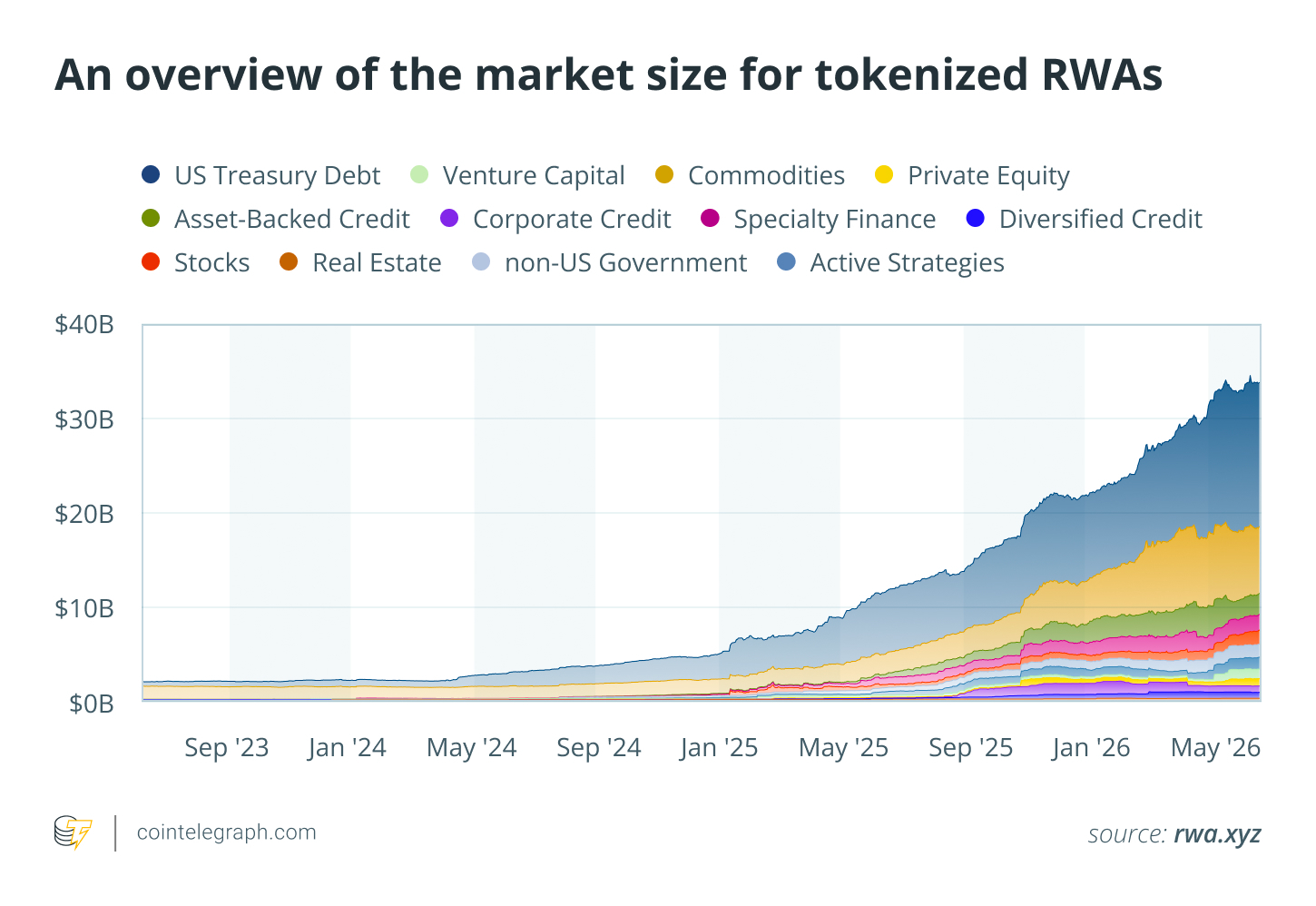

Excluding stablecoins, onchain RWA value has grown from roughly $2.7 billion in January 2024 to about $30 billion in April 2026. Sovereign debt remains the largest segment of RWA at $14.8 billion, while private credit sits at $6.1 billion, commodities at $5.4 billion, and equities at $2.1 billion.

However, the growth of RWAs confirms demand for yield-bearing assets that can integrate with crypto-native capital, but it does not prove that retail access for SMEs has been solved. SMEs typically secure credit with tangible assets such as machinery, equipment, vehicles, inventory, or real estate. But most existing RWA products accept financial collateral such as receivables, treasuries, or crypto-native assets. They also remain restricted through accredited investor requirements, minimum capital thresholds, or mandatory KYC onboarding. For example, Centrifuge’s ACRDX limits participation to non-U.S. accredited investors and requires a $500,000 minimum investment. Ondo Finance‘s tokenized treasury products require KYC verification and block access from several jurisdictions. Canton Network targets regulated financial counterparties rather than open retail participation.

Structured-access hybrid model

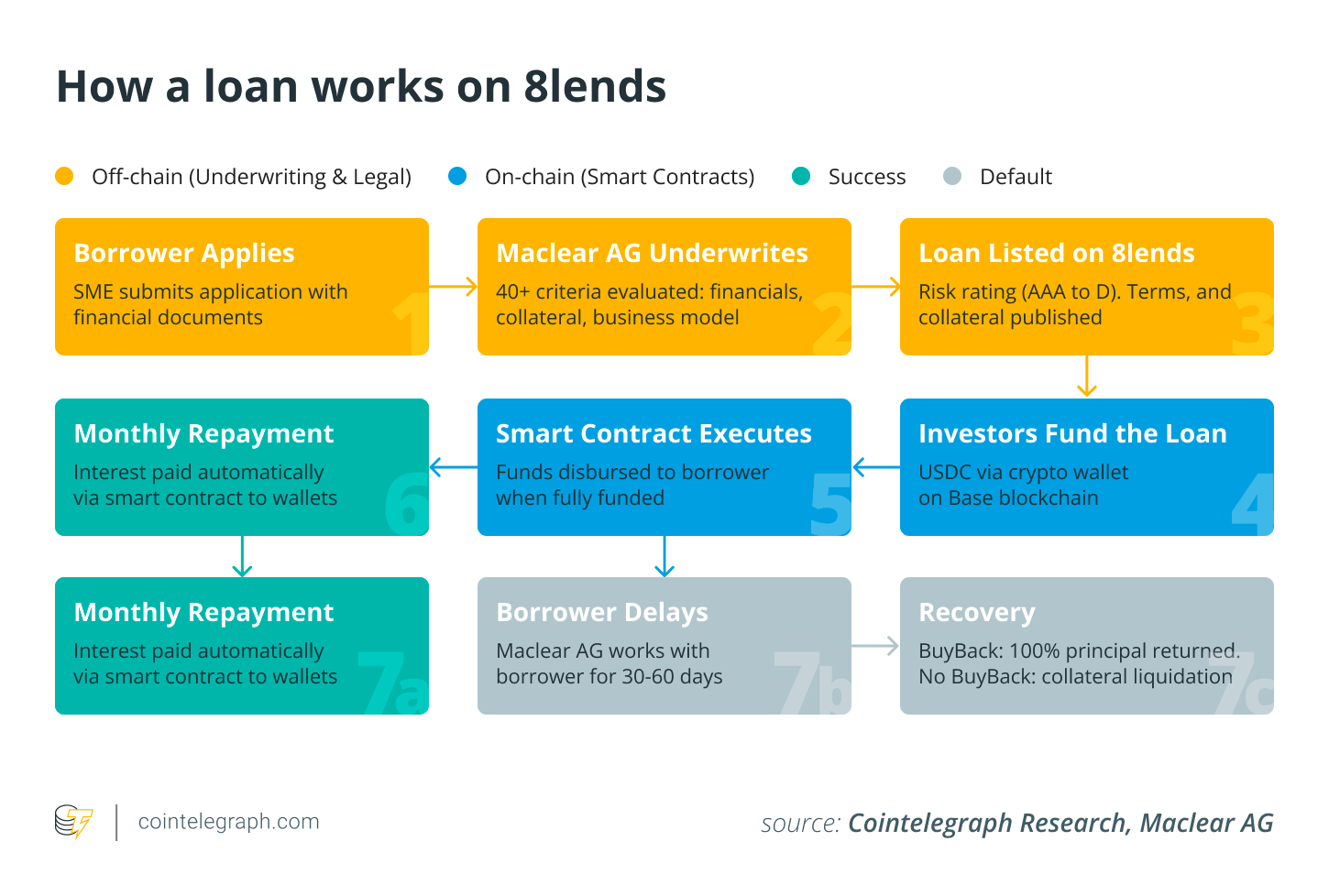

An emerging model under RWA private credit that addresses this mismatch is called the structured-access hybrid model. Under this model, investors deploy stablecoins into smart contracts, which then route capital to regulated lenders that verify borrowers, inspect tangible assets, and enforce legal liens.

One such example of a project building under the structured-access hybrid model is 8lends. It is the retail-facing Web3 interface for Maclear AG, which is a Swiss-registered financial intermediary founded in 2020 and operating as a financial intermediary under PolyReg SRO oversight. In this structure, 8lends functions as the distribution and settlement layer for loans that Maclear originates and underwrites. Investors deposit a minimum of 100 USDC to gain exposure to these SME loans.

As of Q2 2026, 8lends has funded approximately 15.4 million USDC in originations. Of this, 5.79 million USDC has been repaid (~38%) and 9.61 million USDC remains in active credit (~62%), serving 2,143 investors.